Noticing a chill in the market? In the ever-evolving realm of real estate, keeping a pulse on the data is vital. During a recent PLACE Partner Call, our co-founder Chris Suarez unpacked new real estate marketing trends from PLACE investor Goldman Sachs*.

Real Estate Market Trends

The ‘why’ behind high prices

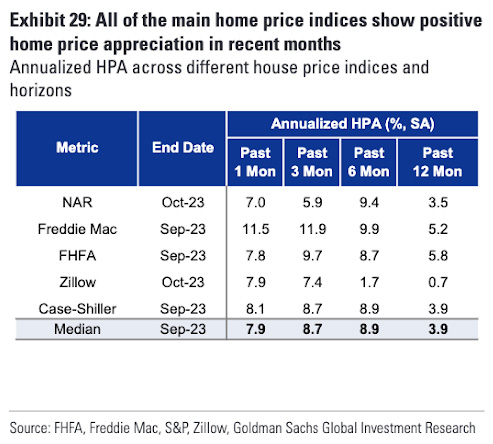

Recent reports highlight a 3.9% year-over-year surge in house prices, signaling a robust market, albeit with nuanced shifts. (See Exhibit 29.)

Industry experts at Goldman Sachs projects home price appreciation of 1.8% and 2.9% in the coming two years, primarily fueled by low housing supply and vacancy rates.

A cooler real estate market

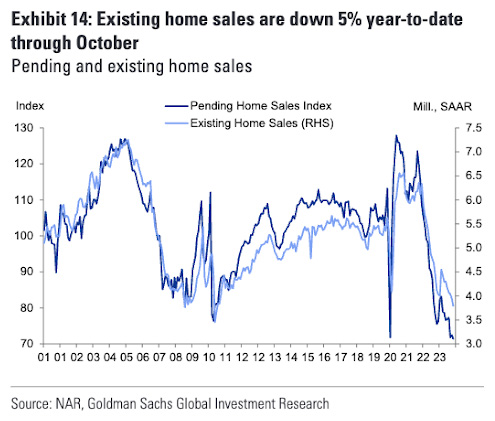

Meanwhile, existing home sales have dipped by 5% year-to-date through October, resting at 3.79 million units. (See Exhibit 14.) This level hasn’t been witnessed since the aftermath of the Global Financial Crisis in 2008 and the continued housing market recession in mid-2010 following the expiration of first-time buyer tax credits.

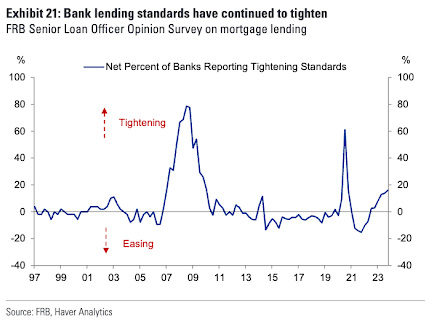

New construction home sales are reverting to pre-pandemic levels, prompting discernible adjustments among builders who are offering incentives and reducing prices to stay competitive.

One of the critical metrics signaling market dynamics is the months’ supply of single-family homes. In October, existing single-family properties saw a slight increase to just over 3 months of housing inventory, while new single-family properties hovered around 7.5 months’ supply. This statistic underscores the delicate balance between housing supply and buyer demand, hinting at potential implications for prospective buyers and sellers alike.

Today’s socioeconomics

1. Personal income, debt are on the rise

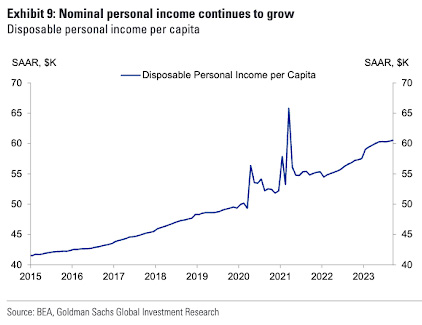

Personal income has remained robust, empowering potential buyers with increased purchasing power. This financial position often plays a pivotal role in driving housing market activities. (See Exhibit 9.)

The current economic outlook presents a mix of opportunities and concerns that ripple through the housing market, impacting potential buyers and sellers. Here’s a snapshot of the key factors shaping the real estate industry:

Adding leverage to your real estate business allows you to grow as a leader. This means leveling up your list of responsibilities and requirements, such as doubling down on your daily activities and production goals to support the level of success that retains a talented real estate agent.

Find ways to nurture your leadership skills through books, webinars, mentorships, or coaching. How you show up affects your relationships and, ultimately, your business. Lead by example, be consistent, and show up more as a guide and business partner.

However, the flip side emerges in the form of a concerning trend – a notable 10% year-over-year surge in credit card debt during Q3 of 2023. This uptick potentially poses challenges for some prospective buyers, tempering their ability to engage in large-scale investments such as purchasing a home.

2. Homeownership is still desirable

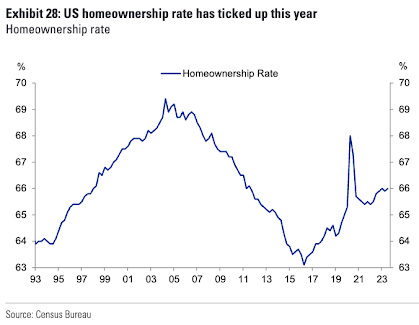

Positive indicators emerge as homeownership rates in the United States are once again climbing, reaching 66%. (See Exhibit 28.) This resurgence signals a favorable inclination towards property ownership, reflecting confidence in the market and stability in the housing sector.

The upswing in homeownership rates, coupled with an increasing pace of household formation, indicates a growing appetite for home ownership.

A solvent society

The lending landscape and borrower behaviors also play a pivotal role in shaping the housing market. Here’s an overview of two key indicators highlighting shifts in credit metrics:

1. FICO scores remain high

A significant marker in the lending landscape is the FICO scores at the time of loan origination. Notably, these scores currently stand at elevated levels compared to the pre-2008 era. This suggests a trend towards more robust creditworthiness among borrowers seeking loans for real estate purchases. Higher FICO scores often indicate greater reliability and creditworthiness, signaling a more stable borrowing environment within the housing market.

2. Debt-to-income ratios trending lower

Another crucial metric, the debt-to-income (DTI) ratio, experienced a decline in Q2 of 2023. This reduction signifies a positive shift, indicating that borrowers are managing their debt more effectively relative to their income. Decreasing DTI ratios often signals improved financial health among borrowers, potentially enhancing their capacity to qualify for property loans and manage their financial obligations more prudently.

Navigating the real estate market in the wake of these fluctuations demands a nuanced understanding. While projections suggest promising growth, the market’s responsiveness to external factors remains unpredictable. Keeping a watchful eye on the supply of houses, mortgage interest rates, and broader economic activity will be instrumental for both buyers and sellers in making informed decisions amidst this dynamic landscape.

*Disclaimer: All data and information is provided “as is” for informational purposes only, and is not intended for trading purposes or financial, investment, tax, legal, accounting, or other advice. We highly recommend you seek professional advice from someone who is authorized to provide investment advice.